Attractive mispricing opportunities in China

- Nick Bird

- Feb 1, 2024

- 7 min read

Updated: Mar 6, 2024

There are numerous equity market dislocations across the broad spectrum of Chinese securities. They are the result of extreme liquidity flows driven largely by foreign investors reducing their exposure to Chinese stocks.

On 17 January 2024, the SCMP reported:

“Investors cut the amount of money set aside for Chinese equities by 12 percentage points to the lowest net underweight in more than a year.”

On 19 January 2024, the Financial Times reported:

“International investors ‘just threw in the towel’ after a speech by Premier Li Qiang at Davos on Tuesday lacked any hint of new government measures to boost the economy or financial markets.”

23 January 2024, Bloomberg reported:

“We pulled our clients out of China,” Alicia Levine, BNY Mellon Wealth Management’s head of investment strategy, said on Bloomberg Television Monday. “The political party is sitting at the top of the corporate structure of every large company and small company in China — very hard to invest that way.”

The last comment is an example of the simplistic views held by many foreign investors.

In our December 2023 newsletter, we observed that investors are being highly selective in expressing their bearish China views, largely ignoring Asian stocks listed outside of China which are highly leveraged to Chinese demand and/or Chinese supply chains.

In this research note, we focus solely on mispricing opportunities across the spectrum of Chinese stocks (‘A’ shares, ‘H’ shares and Chinese ADRs).

‘H’ share discount at historical high

At the time of writing (28 January 2024), all dual-listed ‘H’ shares are trading at a discount to their ‘A’ share listing. Haier Smart Home currently has the lowest ‘A’ share discount (7.45%). The second lowest discount belongs to BYD (8.15%). As we documented in our December newsletter, this is despite the fact Berkshire Hathaway (which owns the ‘H’ share) has been selling its holding and there are a couple of ‘H’ share automobile stocks trading at more than a 65% discount to their ‘A’ share price (Great Wall Motor and Guangzhou Automobile Company). As a side issue, the stock which is currently fourth on the list - WuXi AppTec – will likely move to the top of the list on Monday given its ‘A’ listing was limit down on Friday following news of a proposed bill that would stop it accessing federal contracts, but its ‘H’ share will continue to trade at a discount to its ‘A’ share.

Interestingly, there have been times when ‘A’ shares have, in aggregate been cheaper than ‘H’ shares.

Chart 1 shows the Hang Seng Stock Connect China AH Premium Index since 2014. We have chosen 2014 as the starting point as the China Stock Connect program was announced in April of that year and became operational seven months later in November 2014. Stock Connect is a program that links the stock exchanges in mainland China with the Hong Kong Stock Exchange. It allows mainland Chinese and HK investors to trade eligible stocks listed on each other's exchanges.

Chart 1: Hang Seng Stock Connect China AH Premium Index Source: OQ, Bloomberg

It’s interesting to note that following the announcement of the stock connect program, the index dipped below 100 and then spiked higher following its implementation (another great example of “sell the fact” in financial markets!).

This month the Hang Seng Stock Connect China AH Premium Index hit a multi-year high. We need to go all the way back to the depths of the financial crisis (March 2009) – well before the introduction of the stock connect program - for when the index registered a higher value.

One potential issue with the Hang Seng Stock Connect China AH Premium Index is that it’s cap weighted and driven by large cap stocks, notably the Chinese banks.

At OQ, we prefer to look at a time series of the median ‘H’ share discount (Chart 2). This calculation is performed for all ‘A’/’H’ pairs where the median daily turnover of the ‘H’ share is more than $US2m. This is done to address the criticism that some ‘H’ shares justifiably trade at a large discount due to the lack of liquidity. This analysis also shows that ‘H’ shares are extremely cheap relative to ‘A’ shares.

Chart 2: Median ‘H’ shares discount vs ‘A’ shares Source: OQ, Bloomberg

It’s hard to justify why an ‘H’ share should trade at a substantial discount to its ‘A’ share listing. Both ‘A’ and ‘H’ shares have the same voting rights and dividend entitlements. And since the launch of stock connect in November 2014, mainland investors can easily purchase ‘H’ shares.

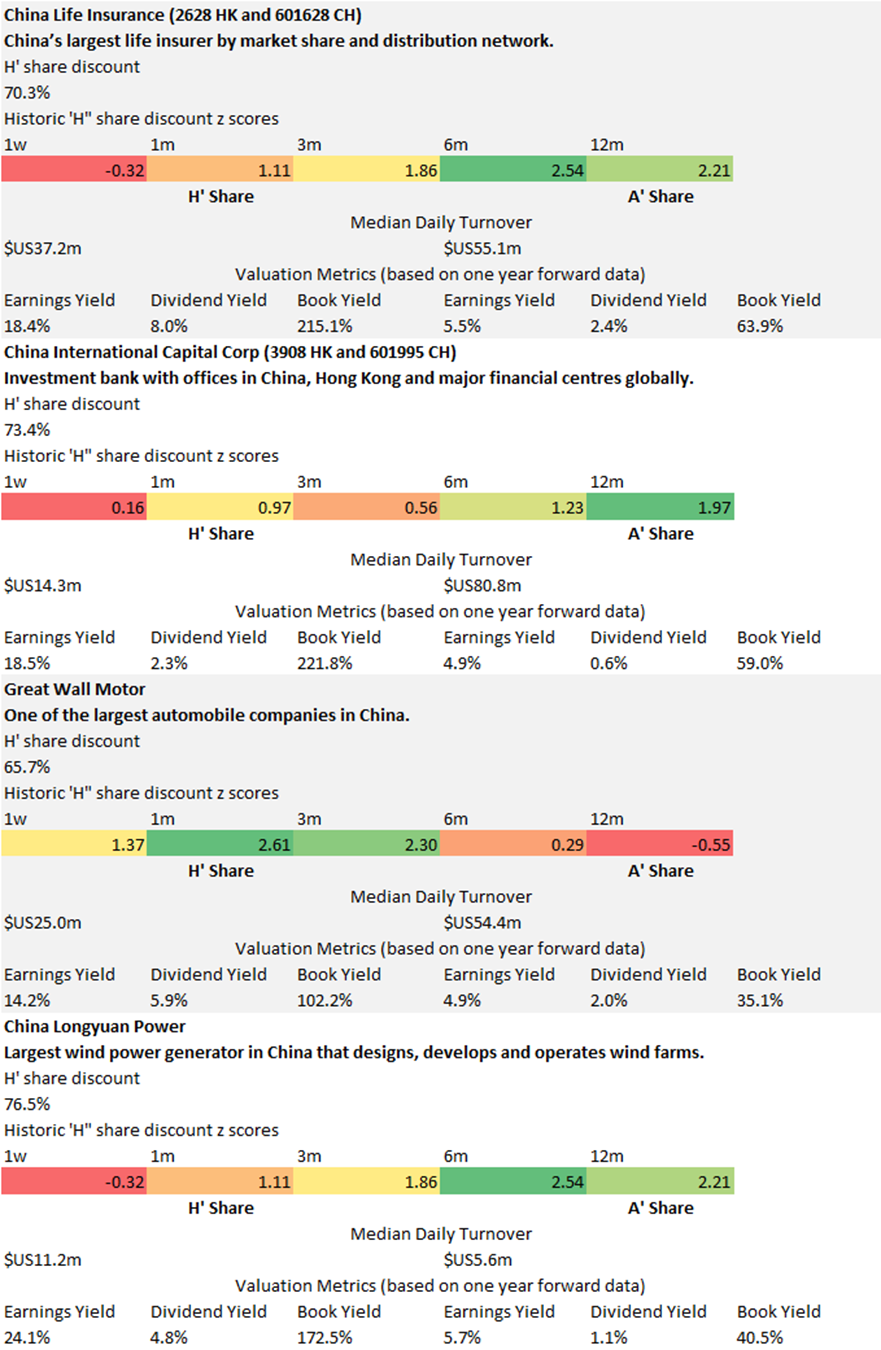

We highlight four extreme stock examples in the table below. In each case, the ‘H’ share has a median daily turnover greater than $US10m, the discount to its ‘A’ share has been increasing, and the ‘H’ share can be purchased for around one third the price of the ‘A’ share (and in some cases even less).

In is interesting to note that, given the same dividend entitlements, these ‘H’ shares have a very attractive carry relative to their ‘A’ share listing. Consider China Life Insurance. The one year forward dividend yield is a robust 8.0% for the ‘H’ share and a relatively measly 2.4% for the ‘A’ share. Hence, after one year the ‘H’ share discount would have to increase considerably from the current (which is already close to its historical high) to justify holding the ‘A’ share rather than the ‘H’ share.

Distressed valuations for Chinese tech stocks

It’s well known that the recent stock rally in the United States has been driven by technology stocks. As reported by the Wall St Journal on 28 January 2024:

“Tech stocks keep climbing, while the other 10 sectors of the index are trading an average of 15% below their all-time highs.”

Chinese tech stocks have not just missed the rally but have moved sharply in the opposite direction (Chart 3).

Chart 3: S&P Technology Index vs Hang Seng Tech Index Source: OQ, Bloomberg

Numerous reasons explain the performance differential, including relatively weak Chinese growth, geopolitical concerns, and regulatory risks.

The last reason has garnered the most interest. I’ve lost count of the number of times I’ve read about the Chinese tech crackdown.

Given we have over 1,200 stocks in the portfolio, we rarely talk about individual stocks. In this instance, we’ll make an exception and discuss three large cap Chinese tech stocks which we believe offer a compelling investment opportunity.

First, we’ll briefly address the regulatory backdrop in China. We’ve discussed this issue previously (https://www.oqfundsmanagement.com/post/chinese-delisting-geopolitical-regulatory-and-other-investability-issues), so we’ll focus on what’s changed recently.

A big recent development was the announcement on December 22, 2023, targeting online gaming. What happened subsequently is – in our opinion – of pivotal importance. On January 3, Reuters reported that the official responsible for the announcement had been removed from his post. And on January 23, Reuters reported that the draft proposed legislation had been removed from the regulator’s website.

We don’t want to second guess how and why this played out, but it seems clear that supporting financial markets is now a key priority, even more important than legislation designed to curb potentially inappropriate corporate behaviour. We believe this points to a favourable rather than a hostile regulatory environment.

This is important because when investors start focussing on stock fundamentals again, we believe the following Chinese tech stocks stand to benefit.

Baidu

The most used search engine in China with almost 80% market share. Also has cloud and AI businesses. It’s often referred to as the “Google of China”.

Satisfies our Net Cash Alpha screen. Cash represents approximately almost half of its market cap.

Using cash to increase shareholder yield via stock buy backs.

Satisfies our Long Value screen. Despite various loss-making businesses, including AI, it is trading on a one year forward earnings yield of 10.4%.

Positive short-term sentiment scores driven by recent earnings upgrades.

Tencent

The world’s largest gaming company based on revenue. Other business services include social networking services, online advertising, and mobile value-added services.

Satisfies our Positive Sentiment, Negative Momentum screen.

One of the top ranked stocks in China based on our Growth composite.

Strong balance sheet and recently it’s been increasing the pace of its stock buybacks.

Alibaba

China’s largest e-commerce company. It also has cloud, food delivery and logistics businesses.

Satisfies our Net Cash Alpha screen. Cash represents approximately one third of its market cap.

Aggressive buyback program. Recently the company has been buying back approximately $1 bn in shares per month.

One of the top ranked stocks in China based on our Growth composite.

One year forward earnings yield is 12.5%.

The value proposition for all three companies is compelling. They have strong growth profiles, are cheap and are actively buying back their shares.

They also have another common trait: underperformance. And while investor sentiment toward Chinese tech stocks continues to be negative, they may continue to underperform.

Fortunately, we hedge our risk exposures and have offsetting short positions to mitigate exposures across various risk dimensions. This has allowed us to generate alpha during the recent market downturn.

Negative ‘H’ share performance compared to Chinese ADRs

There are numerous Chinese ADRs that have dual ‘H’ share listings. They are fungible and hence the share prices always converge (unlike ‘A’ and ‘H’ shares).

For these dual listed stocks, we monitor the difference between the overnight close price of the Chinse ADR and the ‘H’ share price.

There are days when the ‘H’ share price closes above the price implied by the ADR close, and vice versa. Over time, this evens out, and the average next day ‘H’ share return relative to the ADR close is not statistically significant from zero.

Since the start of October 2023, however, ‘H’ shares have, on average, closed below the price implied by the previous ADR close – and the difference has been significant. There are 12 liquid ADR / ‘H’ share pairs that we monitor in Conquest and the average daily closing price ‘H’ share discounts (relative to the ADR) in in the four consecutive months leading up to January 26 were 0.26%, 0.37%, 0.33% and 0.29% respectively. This is the first time there’s been four consecutive average monthly discounts greater than 0.25%.

It's clear from the data that ‘H’ share selling pressure has been driving down share prices, even when the overseas lead from Chinese ADRs has been positive. It is this selling pressure which is generating attractive investment opportunities which we believe will generate strong alpha when the forced selling abates, and fundamentals play a more important role in price discovery.

As an example, we’re currently shorting Chinese ADRs which don’t have ‘H’ share listings, and which look relatively unattractive compared to comparable Hong Kong listed stocks because they’ve been less exposed to the adverse liquidity flows that we’ve witnessed recently.

We’re well positioned to exploit these sorts of pricing distortions given our Asian experience and expertise, and the tools we’ve developed to trawl through reams of data to identify attractive investment opportunities.

Comments