Compelling Pair Trades

- Nick Bird

- May 23

- 5 min read

Updated: May 24

We like pair trades for their balanced risk profile, the ability to analyse them based on current mispricing and its evolution over time, and their strong historical contribution to alpha generation within our investment process.

Recently, however, market liquidity imbalances have pushed many pairs to extremes resulting in significant alpha detraction.

This reflects the current market dynamic, where liquidity flows have become increasingly distorted. Retail investors now exert greater influence over price movements, while institutional capital — much of it managed passively — plays a diminishing role.

While this creates short term performance headwinds, it lays the groundwork for meaningful alpha generation once prices realign with underlying fundamentals and valuations.

For each pair, there is ample inventory available for the short leg, and the borrowing cost is low.

Legend (3396 HK) & Lenovo (992 HK)

Legend Holdings trades at an extremely steep discount to its net asset value, currently around 80%.

Legend has a large stake in Lenovo which is the dominant driver of Legend's NAV and typically the lens through which the discount is assessed. Legend is Lenovo's largest shareholder, and it increased its stake from 31.41% at end-2024 to 32.59% at end-2025.

Despite this, Legend trades at approximately a 50% discount to the market value of its Lenovo stake alone and a discount to Legend’s enterprise value, implying that the market no value to Legend's other assets, which include financial services, agriculture, and venture investments.

A NAV discount can be justified based on limited liquidity in Legend's shares relative to Lenovo, and investor scepticism toward Chinese holding companies.

The issue is whether a discount of 80% can be justified.

The following chart shows the relative share prices of Legend and Lenovo since Legend was listed on the HK exchange.

source: Bloomberg

Since its listing, Legend’s share price has declined by almost 73%, while Lenovo’s has risen by more than 52%. Interestingly, Legend’s share price moved largely in line with Lenovo’s for the first three years after listing, before sharply outperforming in late 2017.

Since then, however, the relative performance of the two stocks has diverged significantly.

Legend may also be viewed as an AI play, given its extensive portfolio of early‑stage technology investments.

At some point in the future, shareholders are likely to recognize Legend as an exceptionally inexpensive way to gain exposure to Lenovo, and the relative share prices will begin to converge

Kingboard Holdings (148 HK) & Kingboard Laminates (1888 HK)

Kingboard Holdings is the parent company of Kingboard Laminates, in which it holds a 73.8% controlling stake.

Despite the parent-subsidiary relationship, the two stocks present a striking valuation divergence. Kingboard Laminates carries a market capitalisation of HK$160.2bn at HK$51.10 per share, while Kingboard Holdings — which owns nearly three-quarters of that business plus its PCB operations — trades at just HK$64.6bn at HK$58.30 per share. This implies that Kingboard Holdings' 73.8% stake in Kingboard Laminates alone is worth approximately HK$118bn at market prices, well in excess of the parent's own market cap.

The following chart shows the relative share prices of the two stocks over the last couple of years.

source: Bloomberg

The two stocks traded in tandem until earlier this year. Kingboard Laminates has dramatically outperformed its parent, Kingboard Holdings, year‑to‑date through May 22, 2026, returning +280% compared with +97% for Kingboard Holdings over the same period.

The divergence has largely been driven by AI‑related sentiment, as Kingboard Laminates is viewed as a pure AI infrastructure play.

Kingboard Holdings’ largest shareholder, Hallgain Management, increased its stake several times in April 2026 — the first month of stake increases this year — bringing its holding to approximately 44.2%.

Both stocks are highly liquid.

Misto (081660 KS) & Acushnet (GOLF US)

Misto's primary asset is a 50.3% stake in Acushnet. This is worth nearly twice Misto's own market cap and more than Misto’s enterprise value.

This implies the market is ascribing no value to the remainder of Misto’s business which comprises the Fila brand segment, including a valuable joint venture with Anta Sports (2020 HK) to manage the FILA brand in Mainland China, Hong Kong, and Macau.

The following chart shows the relative share prices (in USD) of Misto and Acushnet since mid‑last year. The two stocks traded broadly in line until mid‑March, when a considerable divergence began to emerge.

source: Bloomberg

While the scale of Korea’s outperformance is exceptional by any historical standard — with the KOSPI up more than 82% year‑to‑date — this rally has been driven largely by surging demand for Korean technology and materials names linked to the AI supply chain. In contrast, deep‑value plays such as Misto have been overlooked. When market sentiment shifts, there is significant potential for stocks like Misto to deliver strong outperformance.

CATL A-Share (300750 CH) & CATL H-share (3750 HK)

I’ve written extensively about CATL’s H‑share premium relative to its A‑share listing, and I’ll continue to highlight it while this absurd mispricing persists.

As a reminder, A‑shares and H‑shares carry the same voting and dividend rights. Since the introduction of Stock Connect in December 2014, Chinese investors have been able to buy H‑shares, while overseas investors can access A‑shares with relative ease.

The following chart shows CATL’s H-share premium since the H-share listed in 2025.

source: Bloomberg

The premium rose quickly to around 30% after listing. This was driven by tight H-share supply relative to the A-share free float, which made the offshore price more sensitive to demand swings.

At the time, the cost of shorting the H-share was relatively high making it less attractive to target the A-H mispricing.

By November 2025, the premium dropped sharply as the lockup on cornerstone investors approached expiry. H-share liquidity also increased and the cost of borrow declined.

Earlier this year, both the premium and the cost of shorting the H-share increased substantially. There was a short period of time when we couldn’t short additional H-shares and the cost of our existing short position was close to 20% per annum.

Recent H-share placements from the company and its second-largest shareholder Sinopec Hong Kong boosted the H-shares’ liquidity. At the same time, the available inventory increased substantially, and the cost of shorting H-shares declined to 0.35% per annum.

What hasn’t changed is investors’ preference for CATL’s H‑shares, with the H‑share premium rising to near its all‑time high. This doesn’t make sense — why would investors buy the H‑shares when they can purchase the A‑shares at a lower price? And why aren’t more investors arbitraging the A/H discount or premium, given that A‑shares can be shorted easily and cheaply?

The current situation defies logic, and unless one assumes equity markets are fundamentally dysfunctional, the H‑share premium should narrow materially in the coming months.

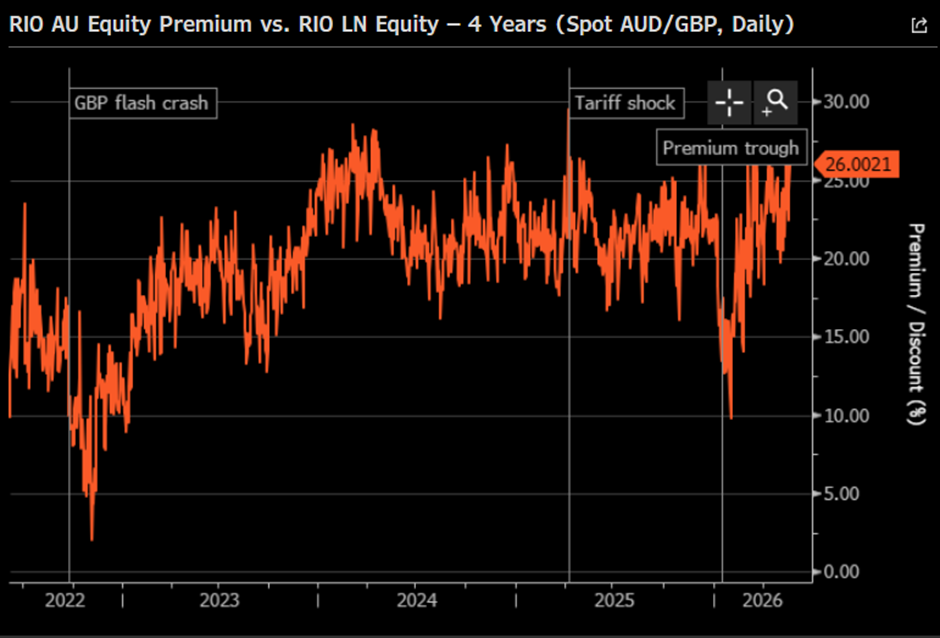

Rio Tinto London (RIO LN) & Rio Tinto Australia (RIO AU)

Rio Tinto has a dual listing in London and on the ASX. The shares are not fungible, and their relative pricing fluctuates over time.

The Australian‑listed shares have traded at a premium to its London listing since around 2010. This premium can be partly justified by the fact Australia’s compulsory superannuation system creates persistent, price insensitive demand for Australian large caps, and Australian investors benefit from franking credits.

Currently, the premium is around 26%. This is very close to the high-end of the range over the last 4 years.

source: Bloomberg

It is worth noting that BHP also operated a dual‑listed structure similar to RIO’s. In August 2021, BHP announced plans to dismantle the arrangement and unify under a single primary listing on the ASX. Shareholders approved the proposal in January 2022, and the unification took effect on 31 January 2022, with BHP Group Limited becoming the sole parent company.

In December 2024, Palliser — an activist investor — formally requisitioned a resolution calling for an “independent, comprehensive, and transparent review” of Rio Tinto’s dual‑listed company (DLC) structure at its 2025 AGMs. Although the proposal was rejected, questions over the effectiveness of the dual‑listing framework are likely to resurface.

Regardless, with the RIO AU premium at extreme levels and near its all‑time high, a long RIO LN and short RIO AU position appears attractive.

Comments